OPINION

Skipped state pension payments undercut workers, economy

By JOHN BURBANK

By JOHN BURBANK

Are you saving for your retirement? If you are working, you are. You put 4.1% of your paycheck into Social Security, through the FICA tax. Now consider if we had no Social Security. The vast majority of workers would be understandably worried about paying the bills on their current income, their co-insurance for health coverage, their mortgage, not to mention saving for college for their kids. Retirement savings? That can be put off another day, month, year, decade. And that is what gets us into trouble when we actually do retire and look for some income to help us along in our declining years.

So we have the people’s pension — Social Security. But even though we all contribute to Social Security, it is no gravy train. The average Social Security benefit is $1,067 a month. We need other retirement savings.

For 66 million Americans, about one out of every three of us, defined-benefit retirement systems provide added income security in retirement. Like Social Security, these systems pool the retirement savings of their members. Their employers also pay into these pools. And in retirement, these pensions provide a solid and dependable monthly check. You won’t get rich, but you will have income security. And that is the point.

Defined-benefit pensions require contributions from both employers and employees. But corporate employers are reducing pension contributions, closing down pension plans, and shifting to deferred compensation, which puts all the cost and burden of retirement on the employees. It’s part of a pattern of disinvesting from workers and their families, channeling more money into profits, outsourcing jobs, and boosting executive pay.

But when Washington state employs people, citizens rightly expect it to model better employment practices than that. After all, we share a public interest in making sure our firefighters, police, public health nurses, teachers, and snowplow drivers can depend on secure retirement income. So governments fund pensions and other benefits (like health care), while keeping public sector wages lower than in the private sector for similar jobs.

In Washington we have developed a series of pension plans for police and firefighters, public employees, teachers, other school employees, and even judges. Because these plans have been well-shepherded, our state is one of the top four in the country with 100% of our combined pension liability funded.

But it is not all roses.

Two pension plans, closed to new employees for almost 35 years, are only funded at about 75% of their liability. That’s in large part because, while workers have been steadily paying into the programs, the Legislature has skipped agreed-upon payments over the past decade.

A couple of weeks ago, the Senate Republicans, along with Democrats Rodney Tom (D-Medina), Tim Sheldon (D-Potlatch), and Jim Kastama (D-Puyallup) proposed a state budget that will dig this hole deeper. They want to completely skip the state’s annual payment into the pension system. That will save the state and local governments $394 million this year. But they will end up paying $867 million later. That’s because at some point they have to make up the skipped payments and the $473 million in lost investment earnings. Talk about bad math.

Other items in the Senate Republicans’ budget don’t add up either: they want to close off the financially healthy current pension programs and push all new employees into a hybrid deferred compensation program. Doing so shifts risk to employees. It also starves the current pension program, because contributions that would have come from new employees are diverted. It boils down to robbing Peter to pay Paul, while undermining a pension system that delivers dependable and modest benefits — the typical benefit is $1,500 a month.

In 2009, state and local pensions generated $4.5 billion in economic output in our state — supporting close to 31,000 jobs, and creating almost $600 million in tax revenues for the federal, state, and local governments. Each dollar invested by the Legislature in pensions supported more than $8 in economic activity in our state.

When you mess around with pensions, and you are messing around with the long-term economic health of our state, with job creation, and the respect and security of retirees.

Washington state has a good retirement system that guarantees a modicum of income security to retired employees. Skipping payments and pushing new employees out undercuts the very people we all count on: teachers, firefighters, police, and others. That may be just another day in the life of a corporation — but those values aren’t shared by most Washingtonians, and they have no place in our state’s budget either.

John Burbank is the executive director and founder of the Economic Opportunity Institute in Seattle. He can be reached at john@eoionline.org.

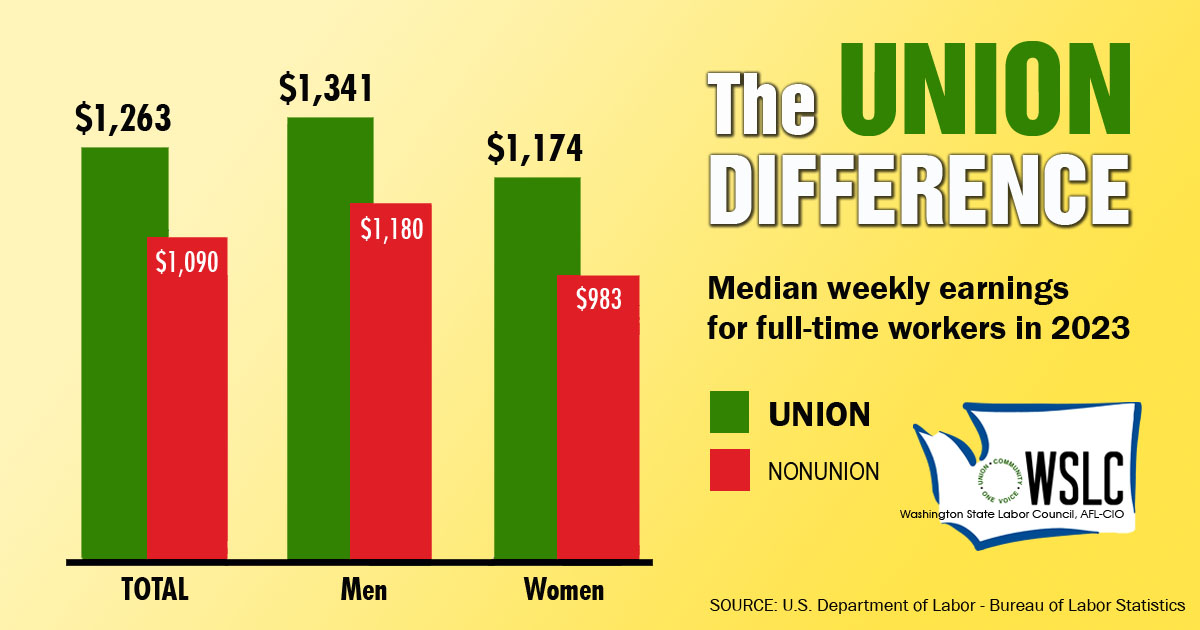

CHECK OUT THE UNION DIFFERENCE in Washington: higher wages, affordable health and dental care, job and retirement security.

FIND OUT HOW TO JOIN TOGETHER with your co-workers to negotiate for better wages, benefits, and a voice at work. Or go ahead and contact a union organizer today!