NATIONAL

Social Security, Medicare report ‘reassuring,’ says Trumka

WASHINGTON, D.C. (June 23, 2016) — Social Security will be able to pay full benefits until 2034, when it will face a modest gap in funding, the social insurance program’s trustees reported on Wednesday. But predictably, corporate media headlines this morning say the situation is “dire” and warn of looming “insolvency” because they want to cut the program’s benefits and/or privatize it to get their hands on some of that money.

WASHINGTON, D.C. (June 23, 2016) — Social Security will be able to pay full benefits until 2034, when it will face a modest gap in funding, the social insurance program’s trustees reported on Wednesday. But predictably, corporate media headlines this morning say the situation is “dire” and warn of looming “insolvency” because they want to cut the program’s benefits and/or privatize it to get their hands on some of that money.

AFL-CIO President Richard Trumka issued the following statement in response to the release of the 2016 Social Security and Medicare Trustees’ Reports:

Today’s reports provide reassuring news for retired and disabled workers, their families and all Americans working toward a secure retirement. But fully funding Social Security’s modest benefits into the indefinite future in the face of a growing retirement income crisis is not enough; and the Medicare report establishes the precipitous growth of prescription drug prices as a major driver of health care costs. These represent some of the most important issues at stake for working people in this election.

Hillary Clinton is committed to strengthening and expanding vital programs working people rely on while Donald Trump can’t be trusted to protect them. We will stand with leaders like Hillary Clinton, so together we control the cost of prescription drugs and improve benefits to ensure that future generations get the retirement security they need and deserve.

Hillary Clinton is committed to strengthening and expanding vital programs working people rely on while Donald Trump can’t be trusted to protect them. We will stand with leaders like Hillary Clinton, so together we control the cost of prescription drugs and improve benefits to ensure that future generations get the retirement security they need and deserve.

Here is a more in-depth analysis by Paul Van De Water of the Center on Budget and Policy Priorities, a nonprofit, nonpartisan research organization and policy institute that conducts research and analysis on a range of government policies and programs:

The financial outlook for Social Security and Medicare has changed little since last year, according to today’s reports from the programs’ trustees. Social Security can pay full benefits until 2034 and Medicare’s Hospital Insurance (HI) trust fund through 2028. The HI trust fund depletion date is two years earlier than last year’s projection but falls within the range that the trustees have projected for some time.

Although both programs face long-run financing challenges that must be addressed, the challenges are manageable. Social Security and Medicare are not “running out of money” or “going bankrupt,” as critics sometimes suggest. Even if their trust funds were to be depleted, Social Security could still pay about three-fourths of scheduled benefits using its tax income, and Medicare HI could pay about 80 percent or more.

The aging of the population is the major driver of the projected growth in Social Security and Medicare. The share of Americans 65 or older will grow by nearly half over the next 25 years as the baby boomers retire. That alone will raise Social Security spending from about 5 percent of gross domestic product (GDP) today to a little over 6 percent of GDP in 2040. Together with rising health care costs, the demographic shift will raise Medicare spending from 3.6 percent to 5.6 percent of GDP over the same period.

Social Security and Medicare benefits are not overly generous. The average Social Security retirement benefit is $16,000 a year, and aged widows and disabled workers typically receive less. Medicare has significant cost sharing requirements and gaps in coverage; as a result, Medicare households spend a much larger share of their budgets on health care costs than other households.

Social Security and Medicare benefits are not overly generous. The average Social Security retirement benefit is $16,000 a year, and aged widows and disabled workers typically receive less. Medicare has significant cost sharing requirements and gaps in coverage; as a result, Medicare households spend a much larger share of their budgets on health care costs than other households.

There is some room to trim Social Security benefits for high earners (and possibly use some of the proceeds to strengthen benefits for particularly vulnerable groups), and policymakers must take further steps to curb the growth of health care costs both in public programs — particularly Medicare — and in the private sector. But even with reasonable efforts to limit their growth, Social Security and Medicare will necessarily require an increasing share of our nation’s resources in the coming decades as the population ages. Social Security and Medicare are highly popular programs, and polls show a widespread willingness to support them through higher tax contributions.

Social Security

The trustees’ 2034 depletion date is for the combined Old-Age and Survivors Insurance (OASI) and Disability Insurance (DI) trust funds, the traditional focus of their report. The two funds are legally separate, however. The trustees expect the OASI fund to remain solvent until 2035. As part of a 2015 budget deal, policymakers extended the solvency of the DI trust fund through 2023 by temporarily allocating to DI a bigger share of the payroll tax. DI needed the additional funds in part because it had been shortchanged following the 1983 Social Security Amendments (which shifted payroll tax revenue from the DI trust fund to the OASI trust fund) even as DI experienced its peak demographic pressures. DI spending, as a share of the economy, has already began to subside from its recent high point, and the trustees project that it will remain fairly stable in the future. Congress will need to revisit DI solvency within the next seven years to avoid an across-the-board benefit cut.

For now, Social Security’s trust funds are still growing. The combined trust fund assets total $2.8 trillion and will grow through 2019. Nevertheless, the population’s aging, which makes more Americans eligible for retirement benefits, means that, even with interest earnings, the trust fund will gradually dwindle after 2019 and be depleted in 2034 if policymakers don’t act by then.

Social Security’s overall shortfall over the next 75 years — 2.66 percent of taxable payroll (the total wages and self-employment income subject to Social Security taxes), or a little less than 1.0 percent of GDP — is virtually unchanged from last year’s estimate of 2.68 percent of taxable payroll.

Although Social Security doesn’t face an imminent crisis, policymakers should act sooner rather than later to restore its long-term solvency. The sooner they act, the more fairly they can spread out the needed adjustments in revenue and benefit formulas over time, and the more confidently people can plan their work, savings, and retirement around those adjustments. Acting sooner also would strengthen the budget as a whole by making progress toward stabilizing the public debt as a share of GDP — a key test of the nation’s fiscal sustainability — and limiting interest costs.

But policymakers must address Social Security reform with great care. The program’s benefits are modest but vital. For two-thirds of elderly beneficiaries, Social Security provides most of their income; for a fifth, it is their sole source of income. Moreover, the scheduled increase in Social Security’s full retirement age — the age at which retirees can receive full benefits — from 66 to 67 between 2017 and 2022 will result in a roughly 7 percent across-the-board benefit cut for everyone who turns 62 after 2022. To avoid harming millions of low-income elderly people and those with severe disabilities, policymakers should restore Social Security solvency through a carefully crafted mix of benefit changes and revenue increases, with the latter contributing a substantial majority of the savings.

Medicare

Health reform, along with other factors, has significantly improved Medicare’s financial outlook. The HI trust fund is now projected to remain solvent 11 years longer than before the Affordable Care Act (ACA) was enacted, and the HI program’s projected 75-year shortfall of 0.73 percent of taxable payroll is much less than the 3.88 percent of payroll that the trustees estimated before health reform. This means that Congress could close the projected funding gap by raising the Medicare payroll tax — now 1.45 percent each for employers and employees — to about 1.8 percent, or by enacting an equivalent mix of program cuts and tax increases.

The trustees’ projections assume full implementation of the cost-control provisions in the ACA, including the Independent Payment Advisory Board (IPAB), and in last year’s Medicare Access and CHIP Reauthorization Act (MACRA). According to the new report, in 2017 the first determination will be made that Medicare growth will exceed the target that triggers IPAB to recommend ways to slow spending, although the projected growth exceeds the target by only about 0.2 percentage points.

The trustees note that the upcoming Social Security cost-of-living adjustment (COLA) is projected to be small and may therefore trigger the hold-harmless provision limiting the increase in some beneficiaries’ premiums for Medicare Supplementary Medical Insurance (SMI). If the hold-harmless provision is triggered, the SMI premium for beneficiaries who are not protected could rise significantly. In such an event, Congress may wish to enact legislation softening the impact, as it did last year in a similar situation. The precise amount of the COLA, however, will not be known until October 18, when the Consumer Price Index for September is released.

Along with directly reducing Medicare costs, the ACA and MACRA payment changes — and payment reforms in the private sector — may encourage structural changes in the health care delivery system that generate further savings. The trustees note that their projections do not assume such additional reductions in health care spending.

Health reform envisions that Medicare will continue to lead the way in efforts to slow health care costs while improving the quality of care. Various research and demonstration projects that the ACA authorizes should yield important lessons. In the meantime, some additional savings can be achieved without ending Medicare’s guarantee of health coverage, raising the eligibility age, or shifting costs to vulnerable beneficiaries. President Obama’s budget includes more than $400 billion in Medicare savings over ten years, and most of these proposals merit policymakers’ support.

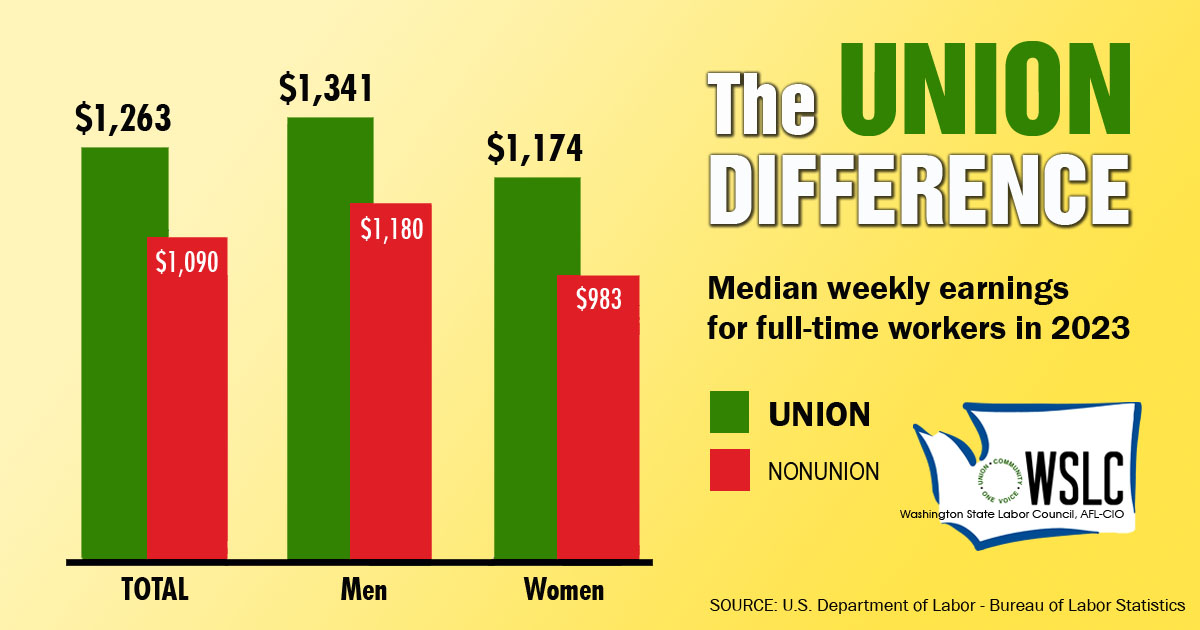

CHECK OUT THE UNION DIFFERENCE in Washington: higher wages, affordable health and dental care, job and retirement security.

FIND OUT HOW TO JOIN TOGETHER with your co-workers to negotiate for better wages, benefits, and a voice at work. Or go ahead and contact a union organizer today!