OPINION

Social Security in Washington state: Facts and fixes

Social Security ensures dignity for millions of Washington residents. Here’s how lawmakers can keep it that way.

By AARON KEATING

Image via Flickr Creative Commons

(Dec. 9, 2019) — Social Security improves the economic security of more than 1.3 million Washington residents and their families, and contributes significantly to economic stability and growth across the state. While it is currently on sound fiscal footing, federal lawmakers should act now to remove Social Security’s cap on taxable earnings, raise benefits and make other improvements to ensure it meets the needs of today’s workers, families and retirees.

Social Security improves economic security, stability and growth in Washington

Social Security provides income for 30 percent of the state’s households. More than 1.3 million Washington residents receive Social Security benefits, representing 18 percent of the state’s population.[1] Of people receiving benefits, 77 percent (more than 1 million) are age 65 or older, 17 percent (230,000+) are age 18-64 and 6 percent (73,000+) are under 18. Nine in 10 residents age 65 or older receive benefits; 55 percent of those (568,000+) are women.[2]

Social Security dramatically reduces poverty among the elderly in Washington. Without Social Security, elderly poverty rates would climb from 7.2 percent to 34.4 percent.[3] Even though average retirement benefits are just $1,490/month ($17,880/year), Social Security kept an estimated 317,000 Washingtonians age 65 or older from living in poverty in 2018.[4]

Social Security is the primary insurance protection for 95 percent of Washington’s 1.8+ million children and families. In the event a parent or spouse were to die or be disabled, more than twice as many children would live in poverty if there were no Social Security benefits.[5][6] In 2018, nearly 108,000 widow(er)s and children in Washington received an average $1,291/month ($15,489/year) for survivor’s benefits; more than 207,000 disabled workers and their families received an average $1,301/month ($15,616/year).[7]

Social Security significantly boosts Washington’s economy. In 2018, benefits were equivalent to 5 percent of state total personal income – generating an estimated $42.3 billion in economic activity, more than 268,000 jobs and nearly $2.2 billion in state and local tax revenue.[8][9] In December of 2018 alone, more than $1.9 billion in Social Security benefits went directly to local economies – from populous King County ($450 million to 295,000 people) to rural Garfield County ($889,000 to 665 people).[10]

Why Congress should “scrap the cap” to bolster the Trust Fund

In the early 1980s, Congress increased payroll taxes and reduced future benefits for millions of Americans in order to build a surplus in the Social Security Trust Fund for the Baby Boomer generation’s retirement.[11] It worked as planned; the latest Trust Fund report projects Social Security can pay all benefits in full and on time until 2035, and three-fourths of scheduled benefits thereafter, even if Congress takes no action.[12]

In the early 1980s, Congress increased payroll taxes and reduced future benefits for millions of Americans in order to build a surplus in the Social Security Trust Fund for the Baby Boomer generation’s retirement.[11] It worked as planned; the latest Trust Fund report projects Social Security can pay all benefits in full and on time until 2035, and three-fourths of scheduled benefits thereafter, even if Congress takes no action.[12]

But lawmakers need to step up. Cuts to Social Security – whether benefit reductions, more limited COLAs, or retirement age increases – will diminish economic security for nearly every American. It will disproportionately affect low- and middle-income families, women and workers of color, who (unlike wealthy individuals) often do not have significant retirement savings and must work further into old age in more difficult and demanding jobs.[13]

To avoid this, Congress should “scrap the cap” to bolster the Trust Fund. Today, workers and employers each pay 6.2 percent of wages to finance Social Security, but there’s a cap on taxable wages ($132,900 in 2019).[14] So while 94 percent of workers pay Social Security tax on every paycheck, most of the earnings of the top 1 percent, and especially the top 0.1 percent, escape being taxed.[15]

Ensuring every American pays the same effective tax rate on their wages would eliminate 85 percent of the Trust Fund’s projected shortfall.[16] Only the richest 6.1 percent of workers (less than 1 in 15) would pay more.[17] And it’s a popular idea: two-thirds of Americans support requiring high-income workers to pay Social Security taxes on all of their wages (as is already the case with Medicare taxes).[18]

How America can create a more equitable and secure retirement for all

As the nation’s most efficient, secure, universal and portable source of retirement income, Social Security has all the advantages (and none of the disadvantages) of both traditional pensions and 401(k)s – and it offers benefits unavailable in the private sector, like automatic inflation adjustments and benefits for divorced spouses.

Federal lawmakers should take steps to expand and improve Social Security for today’s workers and families by:

Raising benefits overall: Adjusting the benefit formula to raise benefits for those who have had careers in low-wage occupations – such as childcare, restaurant service, or home health care – would better protect the financial security of people just scraping by, particularly older women and people of color.

Protecting the very elderly: Living to extreme old age, or living without a spouse greatly increases the risk of poverty. “Bump-ups” in benefits for seniors living past a certain age and increasing benefits for elderly widow(er)s would reduce financial insecurity among these vulnerable people.

Reducing gender and racial inequities: Caring for children or aging family members can cause many people, especially women, to reduce time in the workforce, greatly affecting their retirement benefits. Reducing the number of years’ earnings used to calculate benefits from 35 to 28 can eliminate the caregiving penalty. It would also help those with reduced access to employment due to recessions, discrimination, local economic conditions or disasters, and other barriers.

Restoring student survivor benefits: Before 1981, children of retired, deceased, or disabled workers continued receiving benefits through age 22 if they attended college. Now benefits end once a young person both turns 18 and finishes high school. Reinstating college benefits could help children and their families achieve their dreams, as well as reduce socioeconomic barriers to education and lifetime opportunities.

Adopting the CPI-E inflation index: Over the past decade, Social Security’s existing cost of living adjustment (COLA) formula has led to average increases of about 1.4 percent per year.[19] However, comparatively larger increases in Medicare premiums have often meant many seniors see no additional income from COLAs. Adopting the consumer price index for the elderly, or CPI-E, would more accurately calculate adequate COLAs for retirees.

Restoring office access & services: The Social Security Administration’s (SSA) expenses are self-funded and account for less than one penny of every dollar spent. But from 2010 to 2019, its operating budget fell nearly 11 percent in inflation-adjusted terms — even as the number of Social Security beneficiaries grew by 17 percent. SSA staffing levels have declined by 12 percent since 2010, hampering its ability to perform its essential services.[20] Restoring full funding would help ensure people have dependable and easily accessible in-person service at Social Security offices, often at critical moments in their lives.

Promising federal legislation that needs your support

Congress is considering several measures that would improve Social Security in one or more of the ways outlined above, including: the Social Security 2100 Act (H.R. 860/S. 269), the Social Security Expansion Act (H.R. 1170/S. 478), the Strengthening Social Security Act (H.R. 2654), the Protecting and Preserving Social Security Act (H.R. 2302/S. 1132), and the Social Security for Future Generations Act (H.R. 4121).

Congress is considering several measures that would improve Social Security in one or more of the ways outlined above, including: the Social Security 2100 Act (H.R. 860/S. 269), the Social Security Expansion Act (H.R. 1170/S. 478), the Strengthening Social Security Act (H.R. 2654), the Protecting and Preserving Social Security Act (H.R. 2302/S. 1132), and the Social Security for Future Generations Act (H.R. 4121).

You can send a message here to call on your member of Congress to take action on these and similar bills.

Aaron Keating is Managing Director of the Economic Opportunity Institute. The EOI an independent, nonpartisan, nonprofit public-policy center using research, education and advocacy to encourage public debate and advance new policy ideas that help build an economy that works — for everyone. Learn more at OpportunityInstitute.org. (This column was originally posted at EOI’s blog and is posted here with the author’s permission.)

Aaron Keating is Managing Director of the Economic Opportunity Institute. The EOI an independent, nonpartisan, nonprofit public-policy center using research, education and advocacy to encourage public debate and advance new policy ideas that help build an economy that works — for everyone. Learn more at OpportunityInstitute.org. (This column was originally posted at EOI’s blog and is posted here with the author’s permission.)

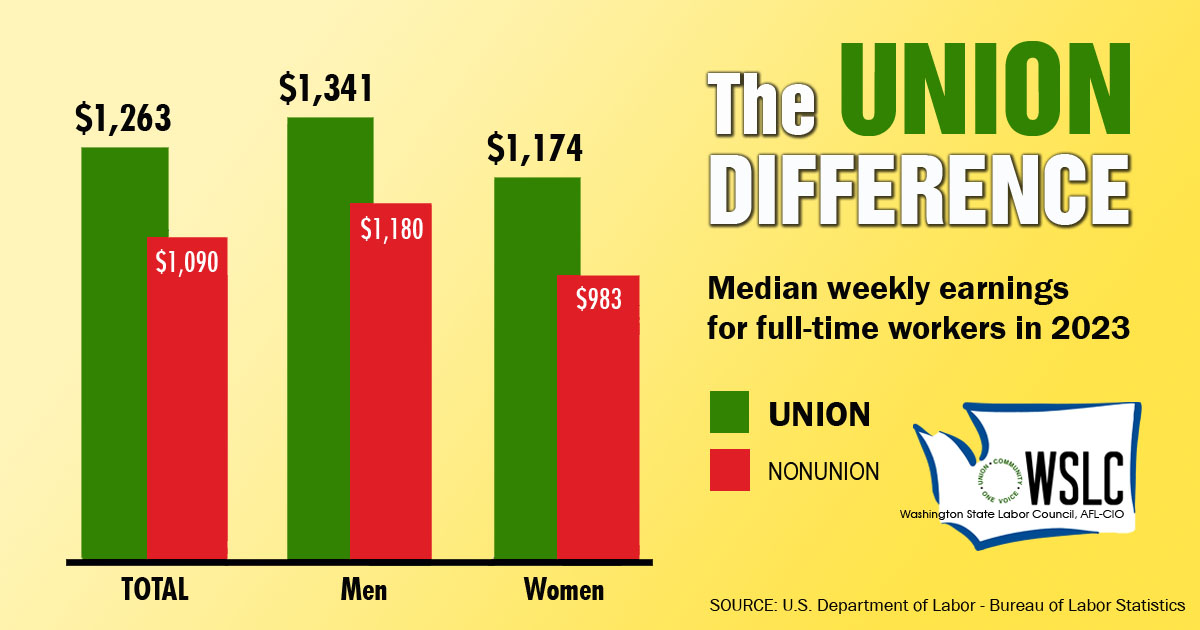

CHECK OUT THE UNION DIFFERENCE in Washington: higher wages, affordable health and dental care, job and retirement security.

FIND OUT HOW TO JOIN TOGETHER with your co-workers to negotiate for better wages, benefits, and a voice at work. Or go ahead and contact a union organizer today!