OPINION

‘Jobs Bond’ would spur state’s economy, private-sector growth

By STEVE ISENHART and JEFF JOHNSON

The timing is right for the Legislature to pass a proposal to build valuable infrastructure projects now at cut-rate prices while laying the groundwork for future economic expansion.

The timing is right for the Legislature to pass a proposal to build valuable infrastructure projects now at cut-rate prices while laying the groundwork for future economic expansion.

The “jobs bond” proposal — for which different drafts have been floated in the state Senate and House — is an ingenious idea to address the devastating construction unemployment rate that is the largest share of the state’s overall jobless rate.

By using small portions of existing (not new) revenue streams, such as the hazardous-substance tax to leverage $1 billion to $2 billion in bonds, we can fast-track the construction of public projects that would have been built anyway over the next several years. By building them sooner rather than later, the state would be able to take advantage of lower construction prices as contractors compete heavily for the relatively few number of construction projects that are currently available.

While the Senate and House outlines differ, the proposal ultimately would fund projects that would improve our quality of life and improve private-sector economic expansion.

For example, as Sens. Derek Kilmer (D-Gig Harbor) and Linda Parlette (R-Wenatchee) noted when distributing their “jobs bond” outline, expanded sewer capacity in a community can often move a private-sector economic-development project from planning to construction.

Moreover, building a new college training facility would not only put people to work at a time when the construction industry is especially hard hit, it would also help ensure we have the ability to train more people for high-demand jobs.

These are responsible investments that do not add to the state’s general obligation debt burden.

Although the “jobs bond” proposal involves debt, that is too simplistic a way to consider it because the payback mechanism for these bonds is already in place. No new taxes would be required, and the how-to-pay decision is not put off for future legislative sessions to wrestle with.

For $1 billion to $2 billion in capital investments now, the proposal would tap very small portions of existing revenue streams such as the hazardous-substance account, the public-works assistance account and the aquatic-lands-enhancement account.

Not only would the “jobs bond” proposal not add to the general obligation debt burden, it would actually help get the state’s operating budget out of its current hole. According to a study by the University of Washington, the construction sector contributes 9% of total state business-and-occupation taxes and 20% of the state’s retail-sales-tax base.

A $2 billion investment would create 30,000 jobs. A third of these would be involved directly in the construction project. The rest are indirect jobs — with manufacturers, suppliers and the corner store selling groceries to re-employed workers.

Today, construction unemployment, depending on the trade, ranges from 20% to 65%. It is clear that the depressed construction industry is holding back employment and state revenue growth. Investing in capital projects now will help to get the state budget back in the black, facilitate private economic growth and get the men and women of the construction workforce back on the job.

Steve Isenhart is president of the Associated General Contractors of Washington. Jeff Johnson is president of the Washington State Labor Council, AFL-CIO. This column originally appeared in the Seattle Times, and is reprinted here with the authors’ permission.

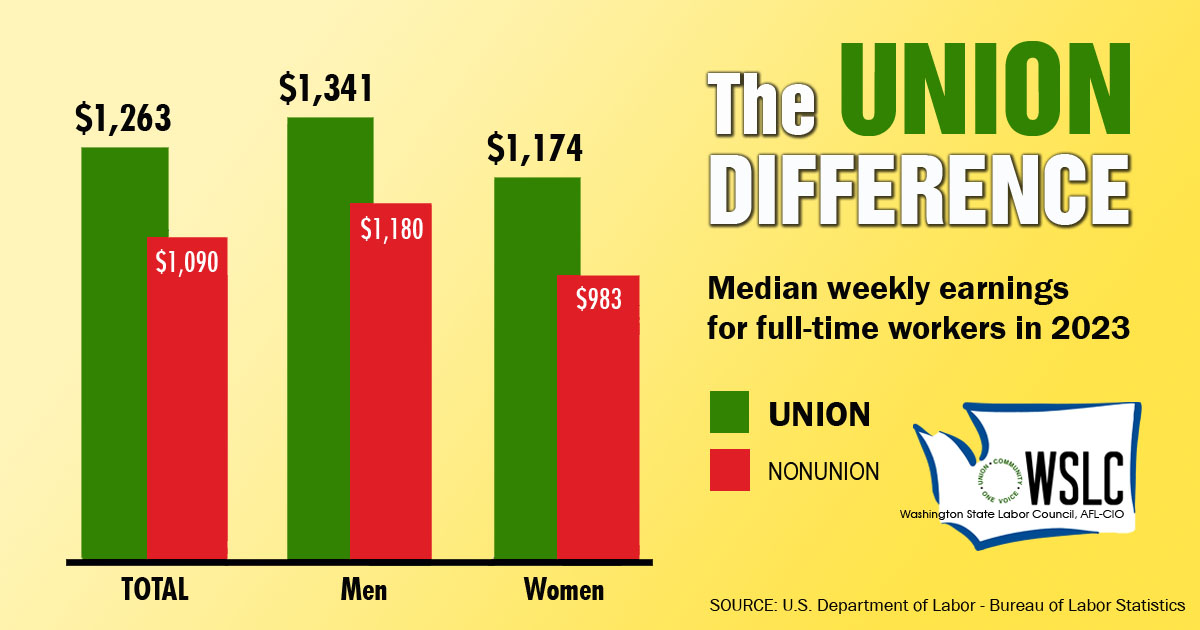

CHECK OUT THE UNION DIFFERENCE in Washington: higher wages, affordable health and dental care, job and retirement security.

FIND OUT HOW TO JOIN TOGETHER with your co-workers to negotiate for better wages, benefits, and a voice at work. Or go ahead and contact a union organizer today!