OPINION

I voted to improve Dodd-Frank reforms, not to ‘gut’ them

By RICK LARSEN

By RICK LARSEN

(Jan. 12, 2015) — As a supporter of Dodd-Frank and someone who was here when Congress wrote it and stood with my communities that suffered as a result of the excess of the financial industry that led to the recession, I can bring a perspective to last week’s vote on H.R. 37 that others can’t.

First, the bill is a collection of 11 separate bills, five of which the House passed overwhelmingly during the 113th Congress. The other six bills cleared their committee votes by large and sometimes unanimous margins. Here is a list with vote totals. I will add here that these bills received next to zero criticism from either party during the last Congress, except for H.R. 4571, which addressed investor disclosures and is separate from the Dodd-Frank Act.

● H.R. 634; passed the House 411-12

● H.R. 677; passed committee 50-10

● H.R. 801; passed the House 417-4

● H.R. 2274; passed House 422-0

● H.R. 742; passed House 420-2

● H.R. 3623; passed committee 56-0

● H.R. 4164; passed committee 51-5

● H.R. 4200; passed committee 56-0

● H.R. 4569; passed committee 59-0

● H.R. 4571; passed committee 36-23

● H.R. 4167; passed House by voice vote

Last year, when the House voted on these bills as a package, 101 Democrats voted against it (I was not one of them). The reason for this opposition is not clear to me when Democrats previously had supported all of the bills except for one.

Second, the last bill on the list above addresses the particular provision from last week’s vote that I think people are upset about. H.R. 4167 passed by voice vote (essentially unanimous passage), and it gave banks until 2017 — basically Congressional blessing of the extended timeline for compliance allowed under the Dodd-Frank Act — to get rid of their collateralized loan obligations (CLOs), financial instruments that pool business loans into securities that are then sold to investors. The vote last week that caused controversy extended this deadline to 2019 for good policy reasons, which I’ll explain.

The Dodd-Frank Act, which became law in 2010, directed financial regulators to write rules about investments that banks could no longer make or hold, and risky trading activities that would no longer be allowed. The Act did not specifically address CLOs.

The five financial regulators responsible for Dodd-Frank issued draft rules in 2011 that also did not address CLOs. After the comment period, they issued a final rule in late 2013 that did include CLOs, and they announced the first of three one-year delays to comply.

This timeline brings us to last Wednesday’s vote, which as I explained above adds two more years to the three the regulators said they intend to give for banks to comply with CLO rules. The anger over this vote seems to have three potential sources:

1. Bills that passed the House or the committee in the 113th Congress with little to no opposition are now garnering more attention than they did last year when they received nearly no attention; or

2. Congress “gutted” a provision in Dodd-Frank, when changing a timeline hardly counts as “gutting;” or

3. Critics want no adjustment to Dodd-Frank. The addition of two years to let banks comply with CLO requirements, on top of the three the regulators said they would grant, hardly seems worth the heat being generated.

Having said all of that, people’s anger at the financial industry is understandable and justified. I share it. I want to see Dodd-Frank implemented well so it has the best chance to succeed in stopping the financial industry from dragging us into another recession. No one likes that these financial instruments are so complex, me included. But it takes time for banks to get them off of their balance sheets. Dumping a bunch of securities into the marketplace could create exactly the kind of instability that Dodd-Frank aims to prevent.

I grant that critics of the vote may have the bumper sticker slogan on their side. However, given what I know and understand about how the rules were written and the actions Congress has taken over the last several years, I would hardly put this vote under the category of “gutting.” When Republicans really start gutting Dodd-Frank, I hope to see at least this much attention paid to it.

Rick Larsen serves as United States Representative for Washington’s 2nd congressional district, a position he has held since 2001. He is a member of the Democratic Party. Contact him here.

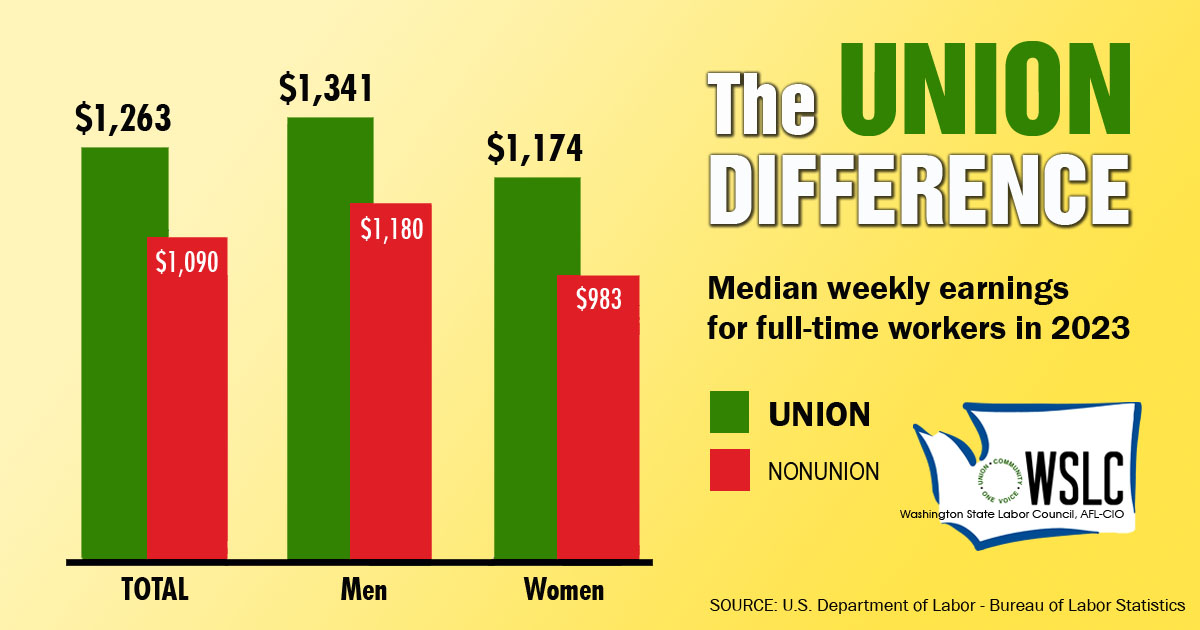

CHECK OUT THE UNION DIFFERENCE in Washington: higher wages, affordable health and dental care, job and retirement security.

FIND OUT HOW TO JOIN TOGETHER with your co-workers to negotiate for better wages, benefits, and a voice at work. Or go ahead and contact a union organizer today!