OPINION

New state law helps employers help workers save for retirement

By JOHN BURBANK

(May 20, 2015) — When you think about retirement, you can imagine a life in which you are freed from decades of work, having to put up with a bad boss or difficult co-workers, be able to take your time waking up in the morning, and go for a walk, a bicycle ride, garden, or just talk to your neighbors and enjoy the local coffee house and tavern.

But the majority of people retiring will not be experiencing a retirement of relative security, enabling them to enjoy their leisure. Most will be retiring into near-poverty.

But the majority of people retiring will not be experiencing a retirement of relative security, enabling them to enjoy their leisure. Most will be retiring into near-poverty.

How does this happen in one of the wealthiest states in one of the wealthiest countries? It doesn’t help that wages have stagnated since the turn of the century or that companies have terminated their defined-benefit pensions, which guarantee a monthly annuity to retirees. The stagnation of wages has resulted in workers not saving for retirement, when their mortgage or rent, utilities, car payments, student debt, and health costs pile up and come first. Half a million Washington citizens between the ages of 45 and 64 have less than $25,000 in savings. And $25,000 in savings will only get you about a monthly annuity of about $160 when you retire.

The end of pensions has taken away a guarantee for income throughout your old age. These pensions did not make retirees wealthy (except for the overloaded retirement products for corporate management), but they did keep retirees economically secure.

The majority of retirees depend on Social Security for two-thirds of their income. The average Social Security check is $1,300 a month. Add the $160 in your savings annuity and your Social Security and you have $1,460 a month, or $17,520 a year, or $48 a day.

Another reason that workers don’t have much in savings is that millions of them can’t save for retirement at work. In our state, 75% of workers who work for employers with fewer than 100 employees can’t make a simple pre-tax retirement savings deduction from their paychecks. That’s because these businesses haven’t set up a retirement plan. It isn’t really their fault. The retirement savings market is flooded with all sorts of companies and products, each of which will claim to be better than the rest.

As an employer, I have gone through the song and dance of financial services companies coming in, each with their own colorful charts. The easiest thing is to throw up your hands. After all, an employer just wants to insure quality and production, find customers, be successful and make a profit. Hassling about the best retirement savings plan is easily pushed off the agenda.

So while we may think that the Legislature is stuck in limbo, it is good to recognize that they enacted a new policy to make it easier for workers and employers to establish retirement savings plans and put money into those plans. This bipartisan legislation, SB 5826, was developed and guided by state Sen. Mark Mullet (D-Issaquah) and Rep. Larry Springer (D-Kirkland). Gov. Jay Inslee signed it into law on Monday.

What does it do? It establishes a Small Business Retirement Marketplace where financial service firms can offer retirement savings products, as long as they meet certain “good business” criteria. They have to offer these products at no cost to employers and they can’t charge more than 1% on the savings of participating employees. The marketplace will enable both employer and employee contributions for retirement.

So if you save 3% of your wages in the retirement marketplace, will it really make a difference? Yes, it does, especially if your employer matches your savings, and you start saving early in your worklife. Starting at age 25, with a wage of $12 an hour, and even with only a 2% increase in wages every year, and even if you get laid off one year in every 10 years, and even if you retire at age 62, you will still gain a monthly annuity from your retirement savings exceeding $1,400 a month. That is $17,500 a year. You will have doubled your Social Security payments. Even if your employer doesn’t match your contributions, you would still have more than $700 a month in this annuity.

That’s a lot better than nothing, better than $160 from your savings, and better than hovering just above poverty.

That’s a lot better than nothing, better than $160 from your savings, and better than hovering just above poverty.

John Burbank is the executive director and founder of the Economic Opportunity Institute in Seattle. John can be reached at john@eoionline.org.

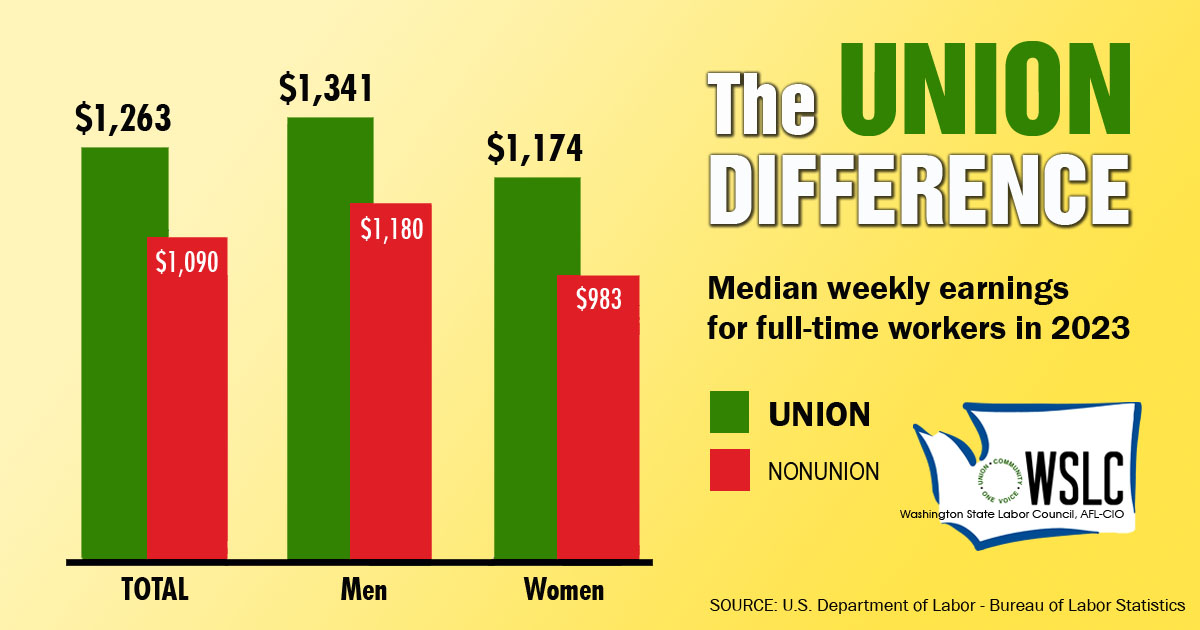

CHECK OUT THE UNION DIFFERENCE in Washington: higher wages, affordable health and dental care, job and retirement security.

FIND OUT HOW TO JOIN TOGETHER with your co-workers to negotiate for better wages, benefits, and a voice at work. Or go ahead and contact a union organizer today!