OPINION

Boeing engineers, America need real retirement security

By JOHN BURBANK

By JOHN BURBANK

Eight years ago, while thousands of corporations were shutting down their retirement plans, the United Methodist Church decided to go back to the future. The Methodists took a lesson from their faith. The Methodist Book of Discipline guides the church in employment practices, and states that the church is “to discharge our fiduciary duty solely in the interests of the participants and beneficiaries, using care, skill, prudence and discipline.” With this in mind, the Methodist established a defined-benefit pension.

What is a defined-benefit pension? It is a plan for retirement that covers all employees in a company. You earn this retirement as you work. You can rest assured that when you retire, you will get a certain amount of money each month for the rest of your life. It won’t get you rich, but it gives you both financial security and peace of mind. That dovetails well with the Methodists, and in fact, with all of us.

Almost all of us are in a defined-benefit pension. It is called Social Security. And it’s the political and financial elite’s favorite punching bag in their assault on entitlements. Never mind that these entitlements are earned. Or that Social Security has been generating surpluses for three decades. Or that it is the most efficient and most effective program to insure retirement security. Or that, unlike almost all other pensions, you can be sure that your Social Security payments keep up with inflation.

Social Security was not meant to provide all our retirement income. That is why unions bargained for retirement plans with big corporations, and why corporations accepted and funded defined-benefit pensions as a traditional part of employment. That deal is now broken. Some 85,000 pension plans have disappeared since 1985. These defined-benefit pensions have been shut down and replaced, if at all, with deferred compensation — also known as 401(k)s.

How’s that worked out? Not so good. If you have a 401(k), just look at your monthly reports over the past five years and you can verify the zigs-zags of value. You might get a bit worried when you think about retiring and you want to make sure you have enough income. The typical value of these accounts is $18,000. That’ll get you about $80 a month.

Why are these annuities so small? It doesn’t take a rocket scientist, or a Boeing engineer, or a Boeing manager to answer this question. Some employers make no contributions. Some do. But they all contribute less than what they would for defined-benefit pensions.

This helps explain why the members of the Society of Professional Engineering Employees in Aerospace (SPEEA) voted down the recent contract offer from Boeing. Boeing proposed to replace defined-benefit pensions with deferred compensation for new employees. The impact of Boeing’s contract proposal would have been to cut its contributions for retirement for these new employees by about 40%. Putting all these employees’ retirement eggs into deferred compensation leaves their accounts at the mercy of the stock market. Even as they gain value, they also create long-term retirement insecurity.

If an employer wants to guarantee retirement income, then it is a lot less expensive through defined-benefit plans rather than through deferred compensation. That’s because with deferred compensation, each individual has to have an account that separately anticipates his longevity. Each individual account has to be enough for a long life for each employee.

Compare this to defined-benefit pensions. These pensions pool all the funding to finance an average employee’s retirement years. All retirees are taken care of. They can depend on their monthly stream of income, no matter how long they live. For instance, at Boeing, if you work 20 years, the minimum retirement benefit is $1,660 a month. The “herd” of the defined-benefit pension protects the individual retiree.

Unfortunately, what corporate elites focus on is the short term, three-month bottom line. With deferred compensation, these companies can avoid all risk, jettison their fiduciary responsibility, and shift some costs onto employees. While that goes over well on Wall Street, it does not provide a good model for long-term profitability in an industry which cannot afford one engineering, machining or computing mistake.

Would you choose to fly in a plane designed, built and tested by a demoralized and angry workforce, or by well-compensated engineers, technicians, and machinists who are proud of their work and not worried about how they will make ends meet when they retire? I would choose the latter, especially when I am 30,000 feet in the air. I am with the Methodists!

John Burbank is the executive director and founder of the Economic Opportunity Institute in Seattle. He can be reached at john@eoionline.org.

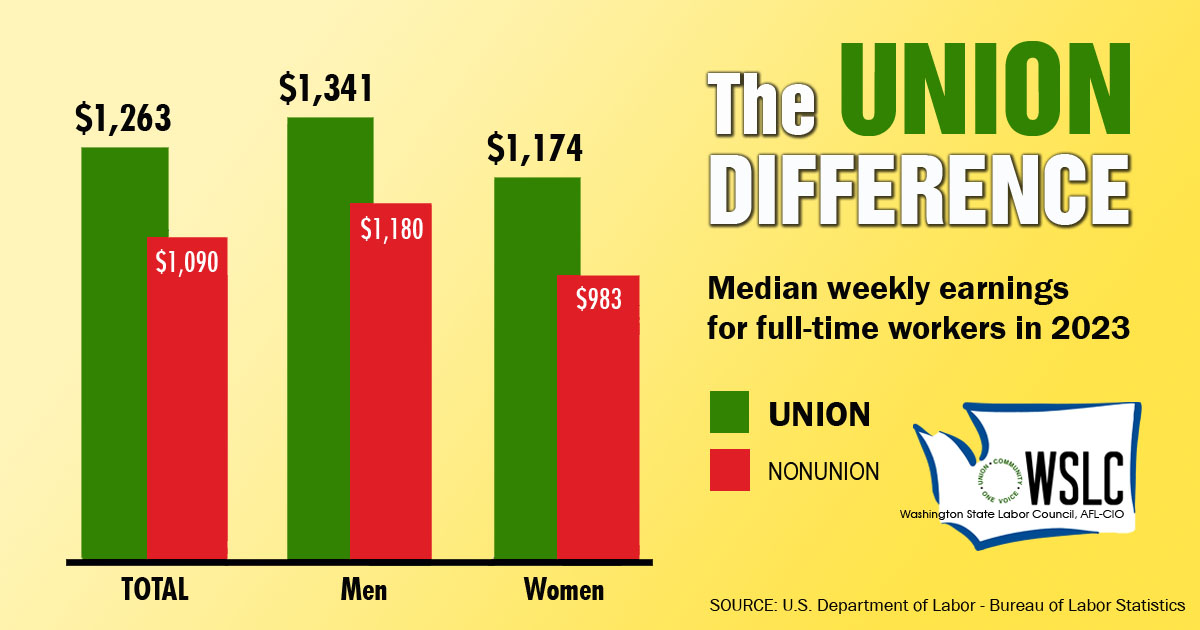

CHECK OUT THE UNION DIFFERENCE in Washington: higher wages, affordable health and dental care, job and retirement security.

FIND OUT HOW TO JOIN TOGETHER with your co-workers to negotiate for better wages, benefits, and a voice at work. Or go ahead and contact a union organizer today!